What If You Cause An Accident? Liability Insurance to the Rescue

Do you work for a company that recently went public? Your stock options and RSUs likely will translate to significant dollars. In this article, you’ll learn about liability protection, a common blind spot for the newly wealthy. You’ll also get tips on how to get liability insurance, and how much you need.

When I work with new clients, most haven’t reviewed their property insurance policies recently. And most are unaware of the risk factors in their everyday lives.

Property Insurance: Overview

There are three types of property insurance. At least one of the three will apply to you:

- Car insurance is required by law.

- Homeowner’s insurance is required by the bank if you have a mortgage. Plus you want insurance to protect this valuable asset.

- Renter’s insurance will protect your belongings, and pay for incremental expenses if you were displaced.

Liability Coverage

The most important component of these three policies is liability coverage, which protects you if you:

- Are at fault for an accident.

- Injure someone else.

- Damage someone else’s property.

- Need an attorney. The liability coverage pays for your legal defense costs if you’re sued as a result of the accident.

Risk Factors

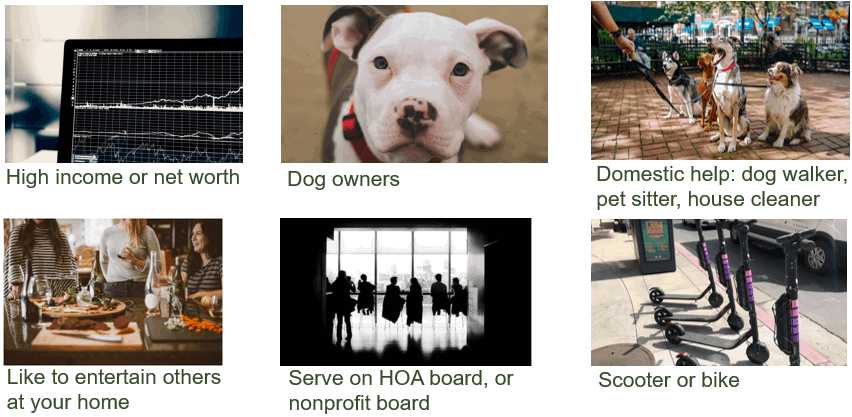

You’re a busy professional woman. You may think you don’t need to worry about risk in your everyday life. But one of the risk factors highlighted above may apply to you.

Let’s say you have a house cleaner who runs a load of laundry and doesn’t notice that it’s overflowing. The water floods and destroys your downstairs neighbor’s unit. You host a dinner party (when the pandemic is over), and your dog bites one of your guests. You’re barreling down Telegraph Ave in Oakland on a scooter, and you seriously injure a pedestrian. Or you’re texting while driving and rear-end a car, causing serious injuries to the other driver.

The “liability coverage” through your homeowner/renter and auto policies protects you if you’re at fault. It also covers your legal fees if someone sues you, including baseless lawsuits.

The liability protection through your homeowner/renter policy follows you. The accident doesn’t have to occur at your home.

How Much Do I Need?

You want the liability protection to be equal to 1-2x your net worth. The maximum liability coverage is $500,000.

{kind=link}