What Should I Do with Company Stock Resulting from RSUs?

Two reasons to sell the shares as soon as the RSUs vest are:

- If you were paid a cash bonus, you wouldn’t use the money to buy company stock. So turn the stock bonus into cash by selling the shares immediately.

- You need to save for short-term goals (e.g., down payment). It’s better to take the sure money by selling now, rather than holding onto the stock for an unknown future stock price.

Depending on your long-term financial plan (the “big picture”), it may make sense to keep or donate the shares.

In my previous post, I discussed RSUs, which are the most common form of equity compensation. Once your RSUs vest, you collect the shares of stock. Let’s assume your company keeps a portion of the shares for the taxes they’re required to withhold on your behalf. You then receive the remaining shares in your brokerage account.

In today’s post, I will discuss whether to keep or sell the shares by addressing two common misconceptions.

Misconception #1: “Keep the Shares Because I’m Optimistic About My Company’s Prospects”

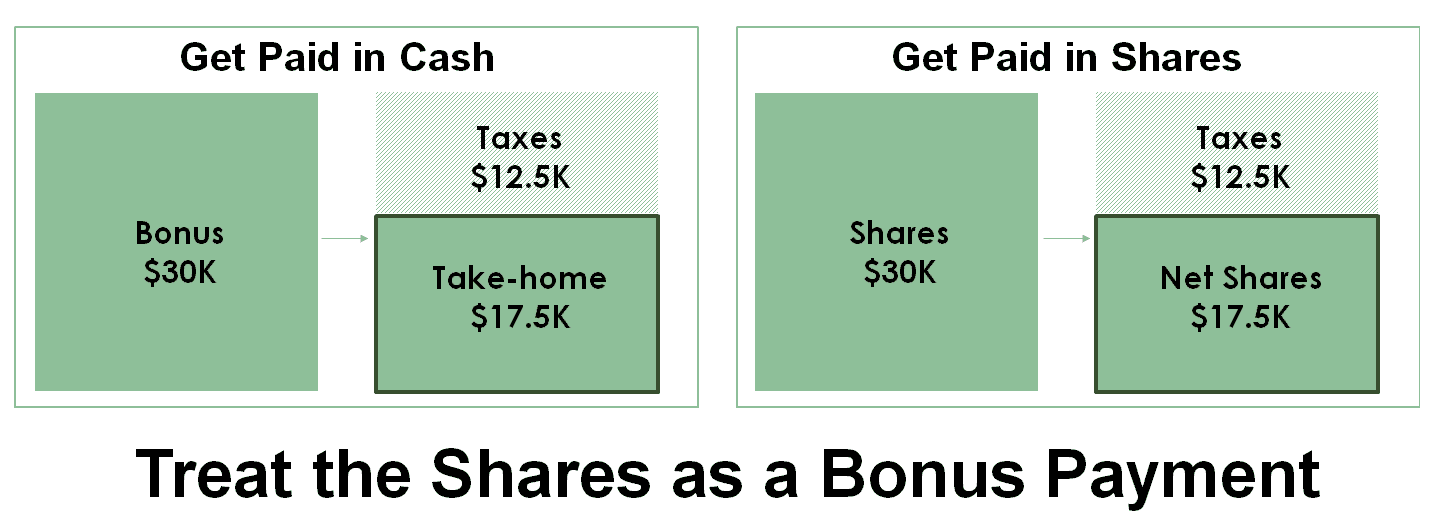

This is a common refrain when clients talk about their companies. It’s possible that your company’s stock price will increase. I help provide clarity by reframing the issue, however: “If your company paid $30,000 cash bonus, would you use this money to purchase company stock?”

Most clients quickly answer, “No, I’d keep the cash.” If you answered “No,” then you should think of the RSU payment as a bonus that happened to be paid in shares rather than cash. In other words, sell all of the shares immediately; your company will withhold taxes, and you keep the remaining cash.

The endowment effect, a behavioral economics term, explains this effect: people will value something that they already own more than a similar item they don’t own. The endowment effect describes people who own company stock and are unwilling to sell those shares, even though they don’t care to buy the stock if they were paid a cash bonus.

In this illustration, compare $30,000 cash bonus (left) vs. $30,000 stock bonus when the RSUs vest (right). In both cases, you pay the same amount of taxes, and you net $17,500 (either in cash, or stock based on the stock price on the vesting date).

If you receive $17,500 cash bonus and would rather use the cash to fulfill other goals rather than purchasing more company stock, then treat the shares as a bonus payment, and convert the shares to cash by selling immediately.

Misconception #2: Keep Shares For 1 Year to “Save on Taxes”

It’s true that when you hold a capital asset for more than one year, long-term capital gains are taxed at a special, lower rate. Short-term capital gains are taxed at regular income tax rates, which are higher.

Reality #1: There Are Two Sets of Taxes

When clients say they want to keep shares for one year, I remind them that there are two sets of taxes to consider:

- You pay taxes on the value of the RSUs at vesting (income taxes)

- You pay taxes again when you sell the shares resulting from the vested RSUs (capital gains taxes)

People focus on the second set of taxes. Don’t forget the first set: you’ve already paid federal and state income taxes based on the stock’s value at vesting.

This is a summary of taxes by phases of the RSU lifecycle (from my previous blog post):

Reality #2: No Savings on State Capital Gains Tax for California Residents

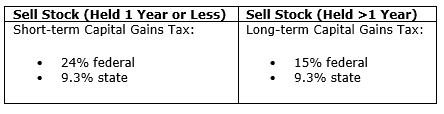

California doesn’t distinguish between short-term and long-term capital gains. Instead, California treats income from selling securities as regular income, as if it were another paycheck.

Let’s say you’re a single filer in California with $175,000 taxable income. Your capital gains tax would be as follows:

The only tax savings from holding the stock for >1 year is on federal capital gains tax. California capital gains tax is the same whether the sale is a short-term or long-term capital gain.

Reality #3: Let Your Goals Determine Whether to Keep or Sell the Stock

Solely focusing on capital gains tax is letting the “tax tail wag the dog”. In other words, beware of letting your focus on taxes distract from your broader goals.

Let’s say you earmarked your company stock for a down payment on your first home. You’re planning to hold onto the shares for one year plus one day to attain long-term capital gains tax treatment. But then the stock price drops 19% (which is what happened to Facebook’s stock price on July 26, 2018). Using the illustration above, if you had sold the shares immediately, you would have pocketed a guaranteed $17,500. Instead, you pocket $14,200, and you’re further from your goal of buying a home (or delay selling the stock and hope the price rebounds, which further exposes you to stock market risk).

Some notable examples of single day stock price drops:

- PG&E (PCG): -52% on 1/14/2019

- Bank of America (BA): -26.2% on 10/7/2008

- Facebook (FB): -19% on 7/26/2018 (this is the largest single day drop based on market cap: $120B loss)

- Microsoft (MSFT): -14.5% on 4/3/2000

- Apple (AAPL): -12% on 1/24/2013

- Google (GOOG): -5.3% on 2/2/2018

What About Old RSUs?

You may have a substantial amount of company stock from past RSUs that vested. Perhaps you held on for a year because you thought you were supposed to (see “Misconception #2”). Or you just never got around to selling shares.

You’re already invested in your company because you work there. It may be too risky to tie your life’s savings to your company stock. For example, if a Bank of America employee had most of her wealth in BAC stock and planned to retire in the fall of 2008, she likely would have been forced to delay retirement for several years. The worst case scenario is for employees of companies like Lehman Brothers and Enron when their companies’ stock price went to $0.

Get the Big Picture

Some people might be able to keep their company stock because they can afford the risk. For example, if a person doesn’t spend a lot of money or wants to work forever, they can attain their financial goals even if their company stock price dropped by a large percentage.

A financial planner can provide this context by running a long-term financial projection to compare:

- What you want (e.g., helping you articulate your financial goals, such as retirement, home purchase, or supporting family members).

- What you have (e.g., your current and future savings).

Keep the Company Stock

If item 2 > item 1, this is a situation where you could keep the company stock. If I had a client in this situation, I would run a “stress test” to gauge the impact of the company’s stock price dropping by 20% or even 100%.

Donate the Company Stock

If item 2 > item 1, and you’re charitably inclined, you can donate stock directly to qualified charities. If you have substantial charitable goals, you can set up a Donor Advised Fund.

Sell the Company Stock

For most people, item 1 > item 2. This is where the art of financial planning comes into play. I help clients find a workable path to attaining their goals. Perhaps they need to delay retirement by a few years, buy a smaller home, or increase their income. This is also a situation where it makes sense to reduce their exposure to the company stock, and reinvest the cash into a diversified portfolio.

Other Considerations

Some publicly-traded companies provide limited dates during which employees are allowed to buy/sell company stock. These are known as “trading windows.” These trading windows usually are quarterly. Trading windows help employees avoid violating federal law prohibiting insider trading. This topic is particularly relevant to executives. If you’re not an executive, it’s worth confirming that you’re not subject to a trading window.

Key employees like C-level executives and VPs must hold a minimum amount of company stock. This is a formula set by the company (e.g., the total value of company stock must be at least 1x base salary).